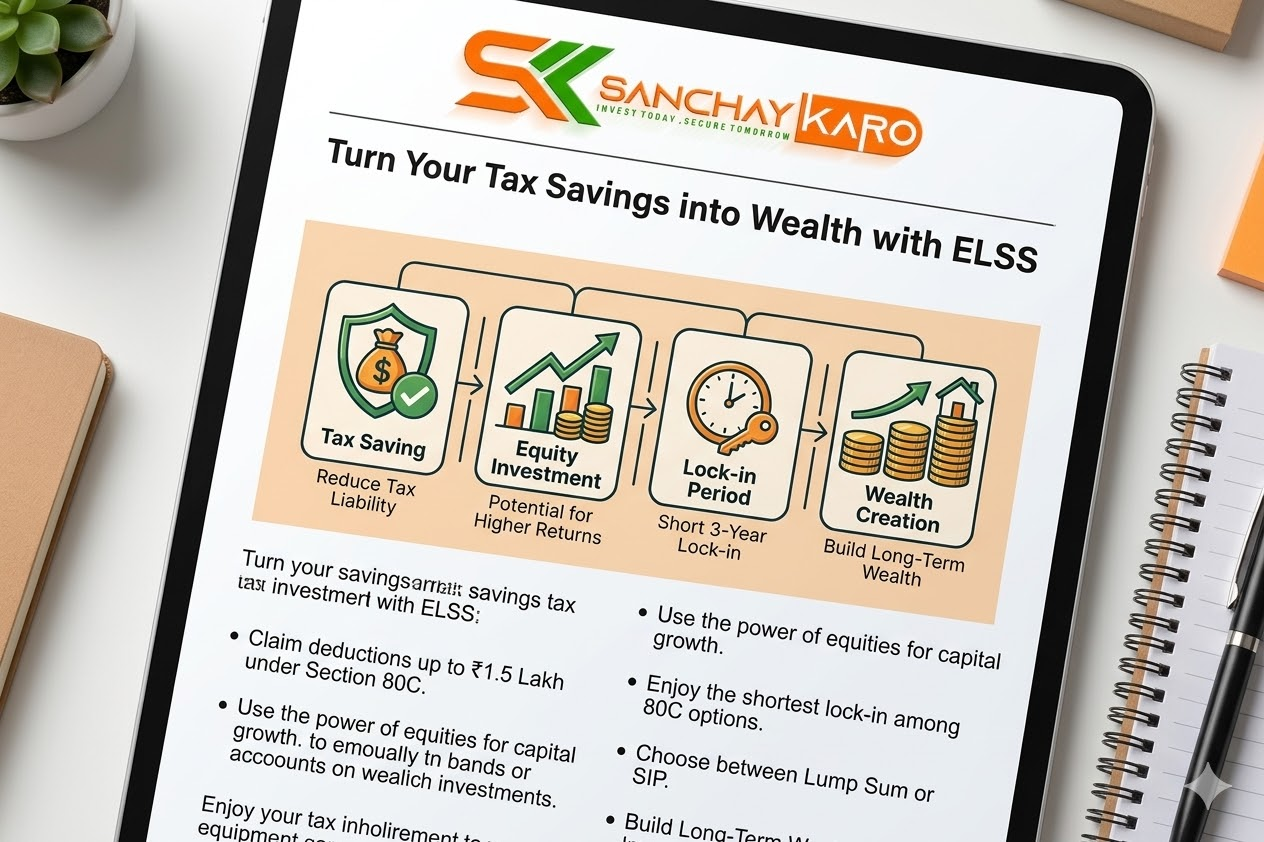

💰 Turn Your Tax Savings into Wealth with ELSS – Save Up to ₹46,800 Annually! (Updated for 2026 Tax Rules)

Hi Sir/Ma’am,

As your dedicated Mutual Fund Distributor, I’m committed to guiding you toward financial success. Whether it’s securing your child’s education, purchasing your dream home, or planning for a comfortable retirement, I’m here to assist you every step of the way.

Before we delve into the exciting world of Equity Linked Savings Schemes (ELSS), I want to inform you that I will be away for a short personal break. During this time, I may not be immediately available, but rest assured, your financial journey continues smoothly. You can still manage and initiate your ELSS investments using the link below:

👉 🎉 Good News!

The Sanchay Karo Investment App is officially LIVE!

Now track & invest in mutual funds anytime, anywhere.

Download now 👇

📲 Android: https://play.google.com/store/apps/details?id=com.rrabbit.sanchaykaro&pcampaignid=web_share

📲 Apple: https://apps.apple.com/in/app/sanchay-karo/id6755289848

Smart Investment. Simple Process. Secure Platform. 🔒📈

Now, let’s explore how ELSS can transform your tax savings into long-term wealth under the 2026 tax rules.

📌 What Is ELSS?

An Equity Linked Savings Scheme (ELSS) is a type of mutual fund that invests at least 80% of your money in company shares (stocks). It offers dual benefits:

- Tax Savings: Under Section 80C of the Income Tax Act, investments up to ₹1.5 lakh are eligible for tax deductions – potentially saving you up to ₹46,800 annually (if you choose the old tax regime).

- Wealth Creation: Being equity-oriented, ELSS has the potential to deliver higher returns compared to traditional tax-saving instruments like PPF or Fixed Deposits.

💡 Why Choose ELSS for Tax Saving in 2026?

1️⃣ Shortest Lock-In Period

ELSS funds come with a lock-in period of just 3 years – the shortest among all Section 80C tax-saving instruments. This means your money is tied up for a shorter duration compared to:

- PPF: 15 years

- NSC: 5 years

- Tax-saving FD: 5 years

2️⃣ Potential for Higher Returns

Historically, ELSS funds have delivered returns ranging from 12% to 15% per annum – significantly higher than traditional options.

3️⃣ Tax on Profits is Low (Updated 2026 Rules)

If you sell your ELSS units after 3 years:

- Long-Term Capital Gains (LTCG) tax: 12.5% (no change from previous year)

- Exemption: First ₹1.25 lakh of LTCG in a financial year is tax-free

- Short-Term Capital Gains (STCG): If sold within 12 months, taxed at 20%

💡 Pro Tip: If your total LTCG from ELSS and other equity investments is up to ₹1.25 lakh in a year, you pay zero tax on those gains!

4️⃣ Flexibility in Investment

You can invest in ELSS through a Systematic Investment Plan (SIP), starting with as low as ₹500 per month. This disciplined approach encourages regular saving and investing.

📊 How Much Tax Can You Save? (2026 Rates)

By investing the maximum allowable amount of ₹1.5 lakh in ELSS, you can potentially save up to ₹46,800 annually – but only if you choose the Old Tax Regime.

| Particulars | Amount |

|---|---|

| Your Investment | ₹1,50,000 |

| Tax Deduction under Section 80C | ₹1,50,000 |

| Tax Saved (30% tax bracket + 4% cess) | ₹46,800 |

⚠️ Important: Old Tax Regime vs New Tax Regime (2026)

As of Budget 2026, there are no changes to tax slabs – they remain the same as last year .

📌 Bottom Line: If you want to claim ELSS tax benefits, you must opt for the Old Tax Regime. Under the New Tax Regime, you cannot claim Section 80C deductions .

🧠 Smart Strategies for ELSS Investment

To maximize the benefits of ELSS, consider the following strategies:

1. Start Early

The earlier you begin investing, the more time your money has to grow. Starting early allows you to benefit from the power of compounding.

2. Invest Regularly

Opting for a SIP allows you to invest a fixed amount regularly, averaging out the purchase cost and reducing the impact of market volatility.

3. Review Annually

While ELSS has a 3-year lock-in, it’s essential to review your investment portfolio annually to ensure it aligns with your financial goals.

4. Plan Your LTCG Exemption

Since the first ₹1.25 lakh of LTCG is tax-free, you can plan redemptions across financial years to minimize tax liability .

📌 Absence Approval Note

As mentioned earlier, I will be taking a short break due to personal reasons. During this time:

- ✅ You can continue or start new ELSS investments using the app link below.

- ✅ For urgent support, my team remains available via WhatsApp or Telegram.

- ✅ All your existing investments are safe, and you’ll continue receiving regular updates.

📲 Start/Continue ELSS – Download SanchayKaro App

💬 Join WhatsApp Channel – For regular updates

📢 Join Telegram Channel – For investment insights

🏁 Final Thoughts: Don’t Let Tax Savings Go to Waste

Tax-saving is a necessity, but why not make it work harder for you? Instead of parking your hard-earned money in low-return instruments, consider channeling it into ELSS funds. Not only will you save on taxes, but you’ll also set the stage for long-term wealth accumulation.

Remember: Under the 2026 tax rules, the ₹1.5 lakh Section 80C deduction is still available – but only in the Old Tax Regime. If you’re already investing in ELSS, PPF, or insurance, sticking with the Old Regime may be more beneficial for you.

The best time to plant a tree was 20 years ago. The second-best time is today.

While I’m away, don’t let your financial progress pause. Take that small step today — your future self will thank you.

Warm regards,

Your Mutual Fund Distributor

Guiding You from SIP to Success

📋 Quick 2026 Tax Summary for ELSS Investors

Disclaimer: Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance is not indicative of future returns. Tax laws are subject to change. Please consult your tax advisor before making investment decisions based on tax implications.