Money in India is more than just currency—it’s a legacy. For generations, we’ve been taught to save diligently, spend cautiously, and view financial discipline as a virtue. These values, passed down from parents and grandparents, come from an era of scarcity where protecting what you had was the ultimate goal.

But times have changed. While our foundations in saving are strong, many of us remain trapped in outdated beliefs that hinder long-term wealth creation. Let’s explore the Indian money mindset, its hidden challenges, and how we can evolve it for today’s world.

Why We Think the Way We Do About Money

Our financial beliefs are shaped by history. Earlier generations faced limited opportunities, job insecurity, and minimal access to financial tools. Their strategy was simple: avoid debt, accumulate gold, buy land, and secure a stable job. This “safety-first” approach became ingrained in our culture.

But in today’s abundant—yet noisy—financial world, clinging solely to these beliefs can limit growth. It’s time to honor the past while embracing tools that match modern realities.

The Fear-Driven Investor

“I don’t want to lose what I’ve built.” This sentiment echoes in countless investor conversations. Fear of loss often leads to overly conservative choices—parking life’s savings in fixed deposits, clinging to traditional insurance plans, or avoiding markets entirely.

While understandable, this fear can be costly. It leads to inaction, missed opportunities, and often, silent wealth erosion due to inflation. True financial safety isn’t about avoiding risk entirely, but understanding and managing it.

Risk vs. Volatility: A Critical Difference

One major misconception is equating market volatility with risk. Volatility is the short-term fluctuation in investment value—like waves in an ocean. Risk, however, is the potential for permanent loss.

Equity investments, including mutual funds, experience volatility. But historically, staying invested over the long term significantly reduces actual risk and harnesses the power of growth. The real danger isn’t temporary dips—it’s never starting at all.

🌱 Start Chota SIP Today!

Small Investment, Big Future ✨

Start investing with amounts as low as ₹100 and build wealth the smart way!

📲 Download the App Now:

Android: https://play.google.com/store/apps/details?id=com.rrabbit.sanchaykaro&pcampaignid=web_share

Apple: https://apps.apple.com/in/app/sanchay-karo/id6755289848

If you are unable to complete KYC by yourself, please fill the Below Form. WhatsApp or call us at 7278480128 – our KYC agent will help you from our end. At that time, you will need to share the OTP you receive from NSE or BSE side.

The Silent Wealth Eater: Inflation

Inflation is the quiet threat most savers overlook. When your returns don’t outpace rising prices, your money loses value over time. Fixed deposits offering 5–6% often barely match inflation, meaning your corpus stagnates in real terms.

From education to healthcare, living costs rise steadily. Beating inflation requires investments designed for growth, not just preservation.

Gold & Property: Comfort vs. Growth

For many Indian families, wealth means gold and real estate—tangible, culturally valued assets. While they have their place, over-reliance on them can create an imbalanced portfolio.

Gold generates no regular income. Property involves illiquidity, maintenance, and market cycles. Modern portfolios benefit from diversification, including financial instruments like mutual funds that offer liquidity, professional management, and growth potential.

Upgrading Your Financial Mindset

Sticking only to traditional methods is like using a basic phone in a smartphone era. Evolving your mindset means shifting from safety-only to purpose-driven investing. Ask: “What is this money for?”而不是 “Is this completely risk-free?”

Goals like a child’s education or retirement need growth—your money cannot afford to sit idle.

Financial Literacy: It’s Simpler Than You Think

You don’t need to be a market expert. Financial literacy means understanding basics: saving vs. investing, how compounding works, tax implications, and how different mutual fund categories serve different needs. Knowledge builds confidence, helps you ask better questions, and puts you in control.

What the Wealthy Do Differently

Wealth isn’t just about high income—it’s about structure. Successful investors set clear goals, follow a plan, review regularly, and practice patience. It’s less about what you earn and more about what you do with it.

Shift from Returns to Goals

Instead of asking, “What return will I get?” start with, “What goal am I funding?” Goal-based investing provides clarity, reduces emotional decisions during market swings, and aligns your portfolio with life’s milestones—education, retirement, travel, or legacy.

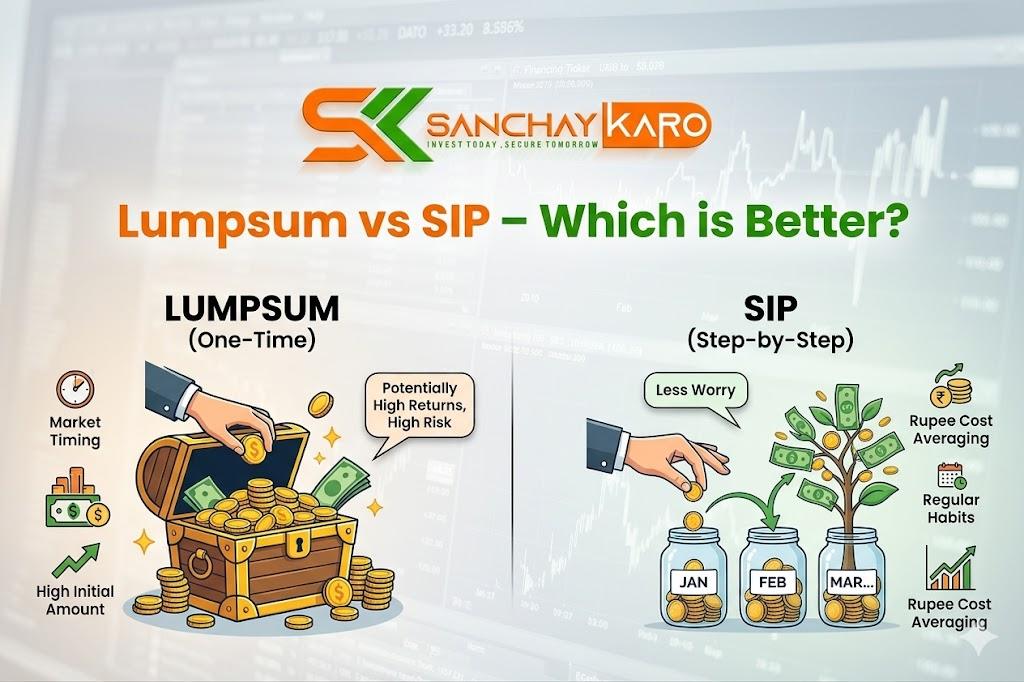

From Saving to Investing

Indians excel at saving. The next step is investing—letting your money participate in economic growth. Mutual funds offer a gateway: equities for growth, debt for stability, and hybrid options for balance, often starting with small, consistent amounts.

Small Habits, Big Wealth

Start small, but start now. A monthly SIP of ₹1,000, sustained over time with compounding, can build significant wealth. Consistency matters more than amount. Compounding is math, not magic—and it rewards those who begin early.

Choose Your Influences Wisely

Surround yourself with voices that focus on long-term planning, not panic or get-rich-quick schemes. Follow educators who simplify finance. Seek advisors who prioritize your journey, not just sales.

Building a Legacy Mindset

True wealth is about freedom, peace of mind, and passing on wisdom—not just assets. Imagine teaching the next generation to invest with clarity, discipline, and patience. That’s the ultimate legacy.