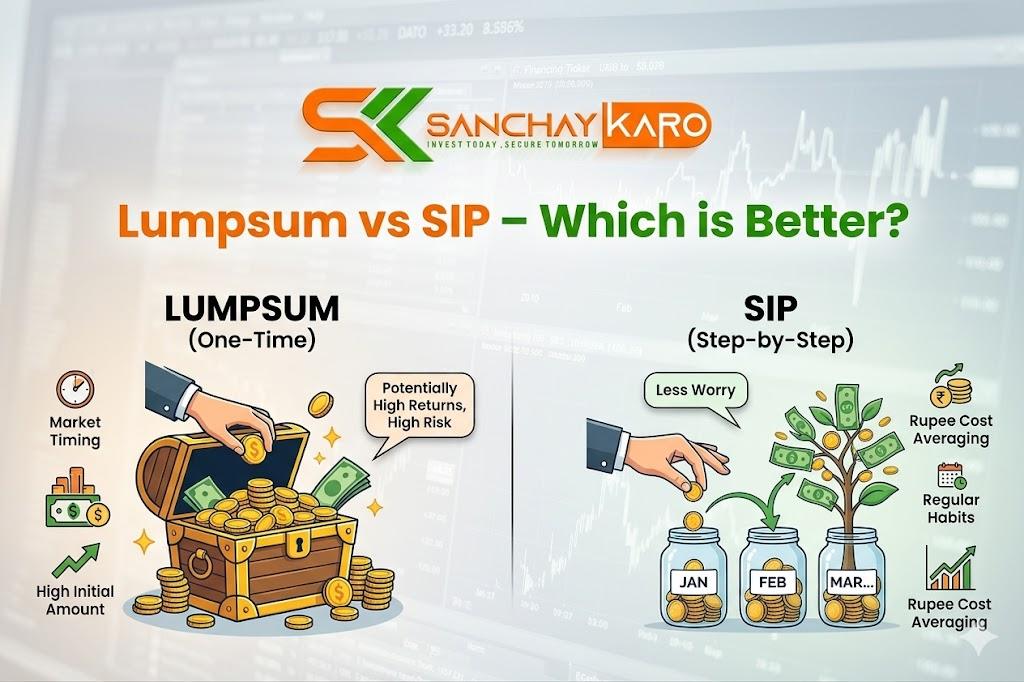

Beat Inflation – Why Fixed Deposits Are Not Enough.FD gives 6%, SIP can give 12% – see the difference.

For generations, Indian families have trusted fixed deposits (FDs) as their go-to investment. The promise of guaranteed returns and zero risk feels comforting. But here’s a hard truth that most banks won’t tell you: FDs are slowly making you poorer.

How? The answer is inflation – the silent thief that erodes your purchasing power every single year. If your money grows at 6% but inflation runs at 5-6%, your real returns are near zero. You aren’t getting richer; you’re just standing still.

Meanwhile, equity mutual funds through Systematic Investment Plans (SIPs) have historically delivered 12% or more over long periods. That difference of just 6% per year creates a staggering wealth gap over time.

Let’s see the numbers with a real-life example.

Investment: ₹10,000 per month for 15 years

| Investment Type | Expected Return | Final Corpus (₹) |

|---|---|---|

| Fixed Deposit | 6% | ₹29,00,000 |

| SIP in Mutual Fund | 12% | ₹50,00,000 |

The difference is shocking: ₹21 lakhs extra with SIP.

You invest the exact same ₹10,000 every month. The FD gives you ₹29 lakhs. The SIP gives you ₹50 lakhs. That’s not a small difference – that’s a life-changing amount. It could be your child’s education, a down payment on a house, or an early retirement fund.

Why FDs Are No Longer Safe from Inflation

Many investors believe FDs are “safe.” But safety has two meanings: safety of principal and safety of purchasing power.

- Safety of principal: Yes, your ₹10,000 will not disappear. The bank guarantees that.

- Safety of purchasing power: No. If inflation averages 5.5%, and your FD gives 6% pre-tax, your post-tax real return is often negative.

Let’s do the math. Assume you are in the 20% tax bracket:

- FD interest rate: 6%

- Tax on interest: 20% → post-tax return = 4.8%

- Inflation: 5.5%

- Real return = 4.8% – 5.5% = -0.7%

You are effectively losing 0.7% of your purchasing power every year. Over 15 years, that loss compounds massively. The ₹29 lakhs you get from the FD will buy far less than what ₹29 lakhs buys today.

The 12% Advantage of SIPs – Not Magic, Just Math

How do mutual fund SIPs deliver 12%? By investing in equities – shares of Indian companies. Over long periods (10+ years), the Indian stock market (Sensex/Nifty) has grown at 12-15% annually. Companies grow, the economy grows, and your money grows with them.

Yes, equities have short-term ups and downs. But for a 15-year horizon, the probability of earning 12%+ is extremely high. Historical data shows that no 15-year period in the Indian market has given negative returns, and the average has been well above 10%.

Breaking Down the ₹21 Lakh Difference

Let’s see year by year how the gap widens between FD and SIP on a ₹10,000 monthly investment.

| Year | FD Corpus (6%) | SIP Corpus (12%) | Difference |

|---|---|---|---|

| 5 Years | ₹7,00,000 | ₹8,20,000 | ₹1,20,000 |

| 10 Years | ₹16,40,000 | ₹23,20,000 | ₹6,80,000 |

| 15 Years | ₹29,00,000 | ₹50,00,000 | ₹21,00,000 |

Notice how the gap accelerates in the later years. Compounding works harder at 12% than at 6%. In the last 5 years alone, the SIP adds nearly ₹27 lakhs compared to the FD’s ₹13 lakhs. That’s the magic of higher returns over time.

But Isn’t the Stock Market Risky?

This is the most common question. Let’s address it honestly.

Yes, equities are volatile in the short term. If you invest for 1-2 years, a market crash could leave you with less than your principal. But for goals that are 5, 10, 15 years away, the risk drops dramatically. No 15-year period in Nifty history has produced negative returns. The worst 15-year period still gave around 6-7% – which matches an FD. The best gave over 18%.

So the real risk is not equities – it’s not investing in equities for long-term goals. By sticking to FDs, you guarantee that inflation will eat your wealth. By choosing SIPs, you give yourself a high probability of creating real wealth.

How to Start Beating Inflation Today

You don’t need to be a stock market expert. You don’t need to time the market. You don’t need a large sum of money. All you need is a SIP in a good mutual fund, and the discipline to stay invested for 5+ years.

Here is a simple action plan:

- Decide your goal: 5 years, 10 years, 15 years – the longer, the better.

- Choose a diversified equity fund: Large-cap, flexi-cap, or index fund. Avoid sectoral/thematic funds if you are a beginner.

- Start a monthly SIP with as little as ₹500 or ₹1,000.

- Ignore market noise – don’t stop your SIP during crashes.

- Increase your SIP every year by 5-10% to supercharge your returns.

Why Sanchay Karo App is Your Perfect Partner

We built the Sanchay Karo Investment App to help everyday Indians break free from low-return investments like FDs and start building real wealth. Here’s how we help:

- Inflation-Beating Portfolios: Our recommended portfolios are designed to target 10-12% long-term returns, helping you stay ahead of inflation.

- Simple Risk Assessment: Answer a few questions, and we tell you the right mix of equity and debt for your goals. No confusing jargon.

- Goal-Based SIP Calculator: Want to see how much you need to invest monthly to reach ₹50 lakhs in 15 years? The app tells you instantly.

- Auto-Debit & Tracking: Set up your SIP once. The app automatically deducts your monthly amount and shows your progress with clear charts.

- Low Minimum SIP: Start with just ₹100. For serious inflation-beating, we recommend ₹5,000 or ₹10,000 monthly, but you can begin small.

- Educational Content: The app includes bite-sized lessons on why FDs are not enough and how SIPs work.

Join Our WhatsApp Community for Smart Investing

Making the switch from FDs to SIPs can feel daunting. That’s why we’ve created the Sanchay Karo Investor WhatsApp Group. Join to:

- Get weekly comparisons of FD vs. SIP returns.

- Ask experts any question about mutual funds.

- Learn from others who have successfully beaten inflation.

- Receive reminders to stay disciplined during market volatility.

👉 Join our WhatsApp group:

https://chat.whatsapp.com/G2Gdsuasv79BJxbGUMdo1u

A Real-Life Story: Ramesh’s FD vs. Sita’s SIP

Ramesh and Sita both started with ₹10,000 monthly at age 30. Ramesh put everything in bank FDs at 6%. Sita started an equity SIP targeting 12%. At age 45 (15 years later):

- Ramesh has ₹29 lakhs. After 5% inflation, his real purchasing power is roughly ₹14 lakhs in today’s money.

- Sita has ₹50 lakhs. Her real purchasing power is roughly ₹24 lakhs in today’s money.

Sita can afford to send her child to a better college, renovate her home, or retire earlier. Ramesh is still struggling to make ends meet. Same income, same savings rate – but completely different outcomes. The only difference was the investment choice.

Your Turn – Start Beating Inflation Today

You don’t have to put all your money in SIPs. A balanced approach is wise: keep 6-12 months of expenses in FDs for emergencies, but invest your long-term savings in equity SIPs. That small shift can add crores to your lifetime wealth.

The ₹21 lakh difference in our example is not a small bonus – it’s a life-changing sum. And it’s available to anyone who chooses smart investing over lazy investing.

CTA: Switch to smart investing. Download Sanchay Karo App and start an SIP.

- For Android: Download from Google Play

- For iOS: Download from the Apple App Store

👉 Join our WhatsApp community for daily smart investing tips:

https://chat.whatsapp.com/G2Gdsuasv79BJxbGUMdo1u

Stop letting inflation steal your future. Start your SIP today.