Beat Low Foreign Bank Interest — Move Your Savings to India SIPs: Your savings account abroad gives 1-2%. India SIPs can give 12%.

If you are an NRI living in countries like the UAE, USA, UK, Singapore, or Canada, you have likely noticed a frustrating reality: the interest rates on your foreign bank savings accounts are near zero. In many developed economies, savings accounts offer 0.5% to 2% at best. Fixed deposits might give 2-4%, often still below inflation. Your hard‑earned money is sitting idle, slowly losing purchasing power.

Meanwhile, India – your home country – offers a completely different story. India’s equity markets have historically delivered 12-14% annual returns over long periods. A well‑chosen Systematic Investment Plan (SIP) in Indian mutual funds can turn your monthly savings into significant wealth.

Many NRIs keep large sums in low‑yield foreign accounts out of habit or lack of awareness. By redirecting even a portion of those monthly savings to India SIPs, you can dramatically increase your returns without taking excessive risk.

A Side‑by‑Side Comparison: $10,000 Over 10 Years

Let’s take a lump sum of $10,000 (or the equivalent monthly savings over time) and see how different strategies perform over 10 years.

| Investment Type | Expected Return (p.a.) | Value after 10 Years ($) |

|---|---|---|

| Foreign Savings Account | 1% | $11,050 |

| Foreign Fixed Deposit | 3% | $13,440 |

| India SIP (Monthly $80) | 12% | $18,400 |

The result is striking: By moving the equivalent of just $80 per month (approx. ₹6,500) into an India SIP, you could end up with $18,400 after 10 years. That is $5,000+ more than keeping the money in a foreign fixed deposit, and nearly $7,400 more than a savings account.

Now imagine scaling this up. If you redirect $500 per month instead of $80, the difference becomes tens of thousands of dollars. Over 20 or 30 years, the gap widens to life‑changing amounts.

Why Are India SIPs So Attractive for NRIs?

India is one of the fastest‑growing major economies in the world. Its equity markets have expanded rapidly, driven by a young population, rising consumption, digital transformation, and structural reforms. While past performance does not guarantee future returns, the long‑term trajectory of Indian equities remains compelling for several reasons:

- Demographic dividend: Over 65% of India’s population is below 35 years, creating a massive workforce and consumer base.

- Formalisation of economy: GST, digital payments, and manufacturing incentives are driving corporate earnings growth.

- Global diversification: For NRIs, adding Indian equities to their portfolio reduces concentration risk (being too heavily invested in one foreign country’s assets).

- Currency advantage: When you invest in India from a stronger currency (USD, AED, GBP, SGD), any appreciation of the INR against your home currency adds to your returns when you repatriate.

But Isn’t Equity Investing Risky?

Every investment carries risk. A foreign savings account is “safe” in nominal terms, but it carries the hidden risk of inflation eroding your purchasing power. A 1% return with 2-3% inflation means you are losing money in real terms.

An India SIP in equity mutual funds carries short‑term volatility. However, for time horizons of 5‑10 years or more, the probability of earning 10‑12%+ returns is very high. Historical data shows that no 10‑year period in the Nifty 50 has produced negative returns, and the average has been well above 10%.

The key is to stay invested and ignore market noise. SIPs automatically average your purchase cost over time, reducing the impact of market timing.

How to Move Your Savings to India SIPs – A Simple Plan

You don’t need to transfer your entire foreign bank balance at once. Here is a practical, step‑by‑step approach:

Step 1: Keep an emergency fund abroad. Maintain 6‑12 months of living expenses in your foreign savings account for immediate needs.

Step 2: Identify surplus monthly savings. Look at your monthly cash flow. How much are you saving after all expenses? Start with a portion – say 30‑50% of that surplus.

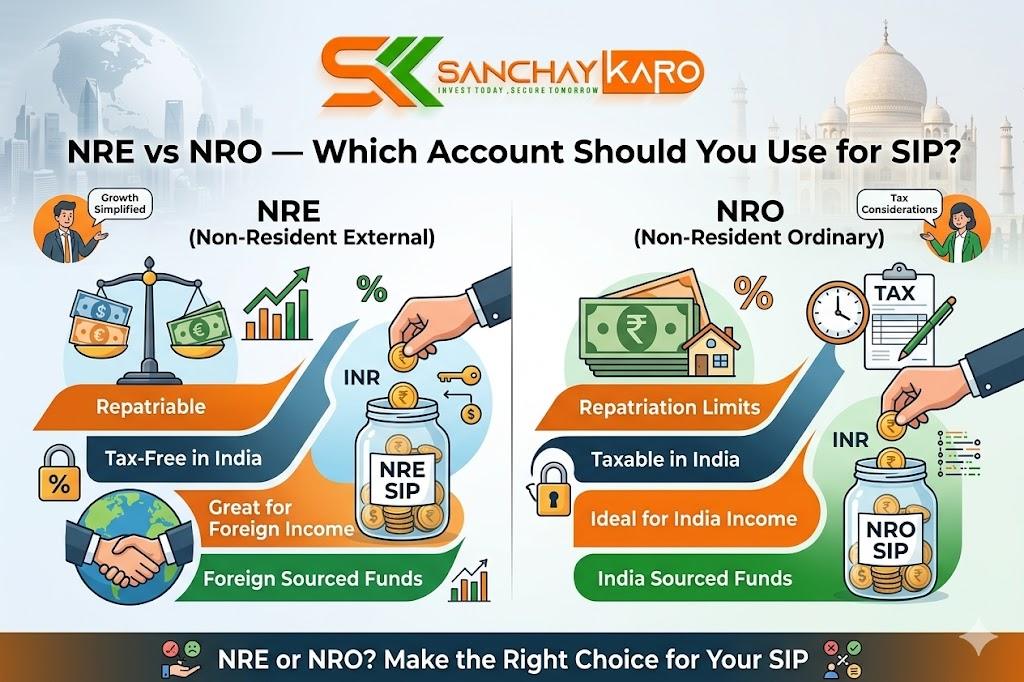

Step 3: Open an NRE account (if you haven’t already). Use your overseas income to fund an NRE account in India. NRE accounts offer full repatriation and tax‑free interest on balances.

Step 4: Start a monthly SIP through Sanchay Karo. Choose an amount you are comfortable with – even $50 or $100 per month is a great start. The app will help you select a diversified equity fund based on your risk profile.

Step 5: Automate and forget. Set up an auto‑debit from your NRE account. Increase the SIP amount every year by 5‑10% (step‑up SIP) as your income grows.

Example: Turning $200 Monthly into a Substantial Corpus

Let’s say you redirect $200 per month (approx. ₹16,500) into an India SIP at 12% returns. Here is what you could accumulate:

| Time Period | Total Investment ($) | Estimated Corpus ($) |

|---|---|---|

| 10 years | $24,000 | $46,000 |

| 20 years | $48,000 | $1,98,000 |

| 30 years | $72,000 | $7,00,000 |

Your $200 per month becomes $46,000 in 10 years and $7,00,000 in 30 years – nearly 10 times your investment. Try getting that from a foreign savings account.

Why Sanchay Karo is the Right Partner for NRIs

The Sanchay Karo Investment App was built to make India investing effortless for NRIs. Here is how we help you beat low foreign interest rates:

- NRI‑friendly onboarding: Complete your KYC digitally using your passport and overseas address proof. No need to visit an Indian bank branch.

- Goal‑based SIP calculator: Enter your monthly savings in dollars (or any foreign currency). The app converts to INR and shows you the future corpus.

- Smart fund recommendations: Based on your risk appetite, time horizon, and repatriation needs, we suggest a portfolio of top‑rated Indian mutual funds.

- NRE/NRO integration: The app helps you open an NRE/NRO account if you don’t have one, and then links it directly for SIP auto‑debits.

- Simple dashboard: Track your investments in INR or your home currency. See real‑time growth and progress toward your goals.

- Step‑up SIP feature: Automatically increase your SIP amount each year – perfect for NRIs who receive annual salary increments.

- SEBI‑registered & secure: Your investments are held with trusted fund houses and custodians. The app is fully compliant with RBI and SEBI regulations.

Join Our WhatsApp Community for NRI Investors

Have questions about moving money from abroad? Not sure which funds to choose? Join the Sanchay Karo Investor WhatsApp Group to connect with other NRIs and experts. Get weekly tips, market updates, and answers to your specific queries.

👉 Join our WhatsApp group:

https://chat.whatsapp.com/G2Gdsuasv79BJxbGUMdo1u

Don’t Let Your Savings Sit Idle

Your foreign bank account is convenient for daily expenses, but it is a poor long‑term wealth builder. By moving even a small portion of your monthly savings to India SIPs, you can earn 12% or more – turning idle cash into a growing asset.

The best time to start was yesterday. The second best time is today.

Download Sanchay Karo App and start earning better returns on your savings.

- For Android: Download from Google Play

- For iOS: Download from the Apple App Store

👉 Learn more about NRI SIPs: Visit our NRI SIP page

👉 Join our WhatsApp community for daily NRI investing tips:

https://chat.whatsapp.com/G2Gdsuasv79BJxbGUMdo1u

Start your India SIP journey today. Your future self will thank you.