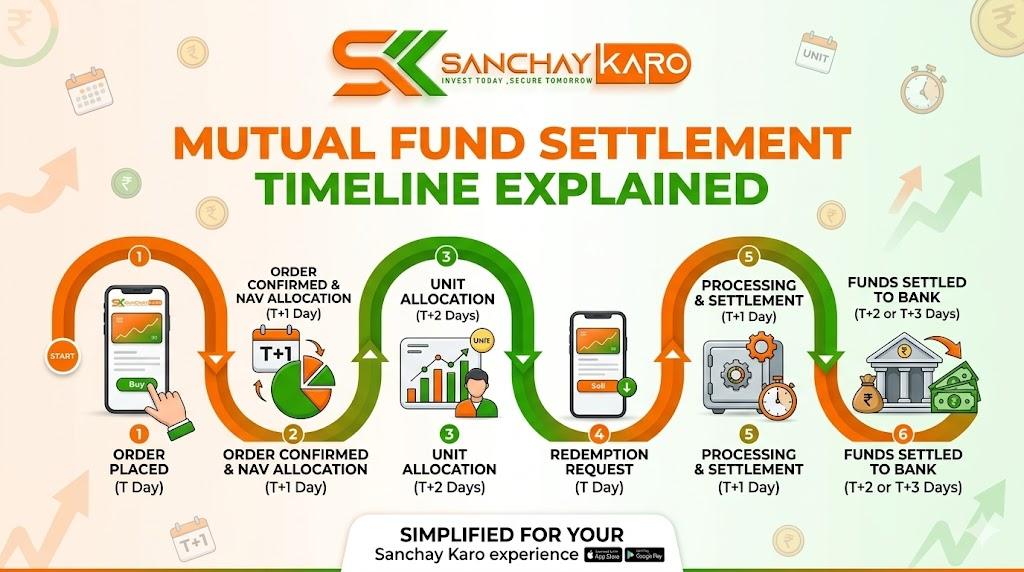

Mutual Fund Settlement Timeline Explained: Why Understanding Mutual Fund Settlement Timelines Matters

If you invest through mutual funds — whether liquid funds, debt funds, equity funds, hybrid funds, index funds, ETFs, overnight funds, gilt funds, global funds, or even a fresh NFO (New Fund Offer) — one question almost every investor asks at some point is: “When will my units actually get credited?” or “When will my redemption money hit my bank account?”

This is where the mutual fund settlement timeline comes into play. The settlement timeline tells you exactly how many days it takes for your purchase (subscription) order to convert into actual units in your folio, and how many days it takes for your redemption order to convert into actual cash in your bank account.

At Sanchay Karo, we believe every investor deserves complete transparency on settlement cycles, NAV allotment rules, RTA (Registrar and Transfer Agent) processing time, and bank credit timelines — so there are no surprises when you invest or redeem.

In this comprehensive guide, we break down the settlement timeline for every category of mutual fund, explain the T+1, T+2, T+3, and T+5 settlement cycles in plain language, and walk through a real-world example so you know exactly what to expect.

What Does “T+1,” “T+2,” and “T+3” Mean in Mutual Fund Settlement?

Before diving into the table, let’s decode the terminology that confuses most first-time investors:

- T stands for the Transaction Day — the day you place your buy or sell (redemption) order, provided it is placed before the applicable cut-off time.

- T+1 means the settlement happens one business day after the transaction day.

- T+2 means settlement happens two business days after the transaction day.

- T+3 means settlement happens three business days after the transaction day.

- T+5 or longer applies mostly to international/global funds and NFOs, where additional processing, currency conversion, or fund-house onboarding steps are involved.

These settlement cycles apply differently depending on whether you are purchasing (subscribing to) units or redeeming (selling) units, and they also vary by fund category — liquid, debt, equity, hybrid, index, ETF, overnight, gilt, global, or NFO.

Mutual Fund Settlement Timeline Table: Purchase vs Redemption

Here is the complete settlement timeline chart across all major mutual fund categories — bookmark this table for quick reference:

| Type of Mutual Fund | Purchase (Subscription) | Redeem (Redemption) |

|---|---|---|

| Liquid Funds | T+1 | T+1 |

| Debt Funds | T+1 | T+2 |

| Equity Funds | T+2 | T+3 |

| Hybrid Funds (Balanced) | T+2 | T+3 |

| Index Funds & ETFs | T+2 | T+2 |

| Overnight Funds | T+0 (Same Day) | T+1 |

| Gilt Funds | T+1 | T+2 |

| Global Funds | T+3 or longer | T+5 or longer |

| NFO (New Fund Offer) | T+5 or longer | T+1 to T+3 |

Settlement Timeline Explained Fund-by-Fund

1. Liquid Funds Settlement Timeline (T+1 / T+1)

Liquid funds are designed for short-term parking of surplus cash, which is why both purchase and redemption settle within T+1. If you invest in a liquid fund today, units typically reflect the next business day, and redemption proceeds are credited to your bank account the next business day too — making liquid funds one of the fastest-settling mutual fund categories on Sanchay Karo.

2. Debt Funds Settlement Timeline (T+1 / T+2)

Debt funds invest in bonds, corporate debt, and government securities. Purchase settles in T+1, while redemption takes slightly longer at T+2, since underlying debt instruments need to be liquidated and RTA confirmation needs to be processed before money is credited back.

3. Equity Funds Settlement Timeline (T+2 / T+3)

Equity mutual funds — including large-cap, mid-cap, small-cap, flexi-cap, and sectoral funds — follow a T+2 settlement for purchase and T+3 settlement for redemption. Since equity markets need time to execute trades, settle stock transactions, and confirm NAV, redemption proceeds for equity funds typically land in your bank account on the third business day after you place the redemption request.

4. Hybrid Funds (Balanced Funds) Settlement Timeline (T+2 / T+3)

Hybrid or balanced mutual funds, which invest in a mix of equity and debt, follow the same settlement cycle as equity funds: T+2 for purchase and T+3 for redemption. This is because the equity portion of the portfolio drives the settlement timeline.

5. Index Funds & ETFs Settlement Timeline (T+2 / T+2)

Index funds and Exchange Traded Funds (ETFs) that track benchmarks like Nifty 50 or Sensex settle both purchase and redemption within T+2, offering a relatively quicker redemption cycle compared to actively managed equity funds.

6. Overnight Funds Settlement Timeline (T+0 / T+1)

Overnight funds are the fastest-settling mutual fund category. Purchases can settle on the same day (T+0), and redemptions settle by T+1, making overnight funds ideal for investors who need ultra-short-term liquidity with minimal settlement delay.

7. Gilt Funds Settlement Timeline (T+1 / T+2)

Gilt funds, which invest predominantly in government securities, follow a T+1 purchase and T+2 redemption settlement cycle — similar to debt funds, given their lower-risk, government-backed underlying instruments.

8. Global Funds (International Funds) Settlement Timeline (T+3 or longer / T+5 or longer)

Global or international mutual funds invest in foreign markets and securities, which involves currency conversion, foreign exchange settlement, and cross-border regulatory checks. This is why purchase can take T+3 or longer and redemption can take T+5 or longer — among the longest settlement timelines in the mutual fund industry.

9. NFO (New Fund Offer) Settlement Timeline (T+5 or longer / T+1 to T+3)

During an NFO, the fund house is collecting fresh investments to launch a new scheme, so unit allotment can take T+5 or longer. However, once the NFO closes and the scheme reopens for ongoing transactions, redemption typically normalizes to T+1 to T+3, depending on the underlying asset class of the new fund (equity, debt, or hybrid).

Real-World Settlement Timeline Example: Equity Mutual Fund Purchase

Understanding the theory is one thing — seeing it play out in real life makes it much clearer. Here’s a practical example of how the equity fund settlement timeline actually works on the ground:

Scenario: You place a buy order for an Equity Mutual Fund on Monday within market hours (e.g., 11:00 AM, before the cut-off time).

- The units are typically credited by Wednesday (first half of the day), following the standard T+2 purchase settlement cycle for equity funds.

- The RTA (Registrar and Transfer Agent) then shares the confirmed allotment details with the platform by Thursday morning.

- This is when the transaction and units get fully updated and visible on your Sanchay Karo dashboard.

So while the technical settlement happens on T+2 (Wednesday), the visibility of units on your app may reflect a day later (Thursday) simply because of the RTA’s data-sharing and reconciliation timeline — not because your money or units are delayed. This is a normal part of how mutual fund settlement and reporting works across the industry, and Sanchay Karo always reflects RTA-confirmed data to ensure accuracy.

Why Settlement Timelines Vary Across Mutual Fund Categories

Several factors influence why one fund settles faster than another:

- Underlying Asset Class – Liquid and overnight funds hold short-term, highly liquid instruments, so they settle quickly. Equity funds need stock market trade settlement, which takes longer.

- Market Liquidity – Debt and gilt instruments are generally less liquid than money-market instruments but more liquid than equities.

- Currency & Cross-Border Processing – Global and international funds require forex conversion and foreign custodian confirmations, extending settlement time.

- NFO Allotment Process – During an NFO, fund houses collect bulk applications and allot units only after the offer period closes, which naturally takes longer.

- Cut-Off Time Compliance – Orders placed after the cut-off time (commonly 1:00 PM–3:00 PM depending on the fund category) are processed as the next business day’s transaction, shifting the entire settlement timeline by one day.

- RTA Processing & Reconciliation – Even after settlement, RTAs like CAMS and KFintech need time to reconcile and share confirmed data with distribution platforms like Sanchay Karo.

Tips to Avoid Settlement Delays on Sanchay Karo

- Always place purchase or redemption orders before the applicable cut-off time to ensure same-day transaction processing.

- For liquid and overnight funds, place orders early in the day if you need faster settlement.

- For equity, hybrid, and ETF redemptions, plan around the T+2 to T+3 settlement window when you need funds for an upcoming expense.

- For global funds and NFOs, build in extra buffer time (T+5 or longer) since these involve additional processing layers.

- Keep your bank account and KYC details updated on Sanchay Karo to avoid redemption credit failures due to mismatched account information.

Frequently Asked Questions (FAQs) on Mutual Fund Settlement Timeline

Q1. What is the settlement timeline for equity mutual funds? Equity mutual fund purchases settle in T+2, and redemptions settle in T+3.

Q2. How long does it take to redeem a liquid fund? Liquid fund redemptions typically settle within T+1, making them one of the fastest redemption categories.

Q3. Why do global mutual funds take longer to settle? Global and international mutual funds involve currency conversion and foreign market settlement, which extends the timeline to T+3 or longer for purchase and T+5 or longer for redemption.

Q4. What does T+2 settlement mean in mutual funds? T+2 settlement means the transaction (purchase or redemption) is finalized two business days after the day the order was placed.

Q5. How long does an NFO take to allot units? NFO unit allotment can take T+5 or longer, since fund houses process applications only after the offer period closes.

Q6. Why do units sometimes appear a day after the official settlement date? This is usually because the RTA needs time to confirm and share allotment data with the investment platform, even though the actual settlement happened on the scheduled T+1, T+2, or T+3 date.

Final Thoughts

Knowing the exact mutual fund settlement timeline — whether you’re investing in liquid funds, debt funds, equity funds, hybrid funds, index funds, ETFs, overnight funds, gilt funds, global funds, or participating in an NFO — helps you plan your cash flow, redemptions, and financial goals far more effectively.

At Sanchay Karo, our goal is to make mutual fund investing simple, transparent, and timeline-friendly for every Indian investor. Download the Sanchay Karo app today and track your purchase and redemption settlement status in real time.

Disclaimer: Mutual fund investments are subject to market risks. Settlement timelines mentioned above are indicative and may vary slightly based on fund house policies, RTA processing, bank holidays, and SEBI regulations. Please read the scheme-related documents carefully before investing.