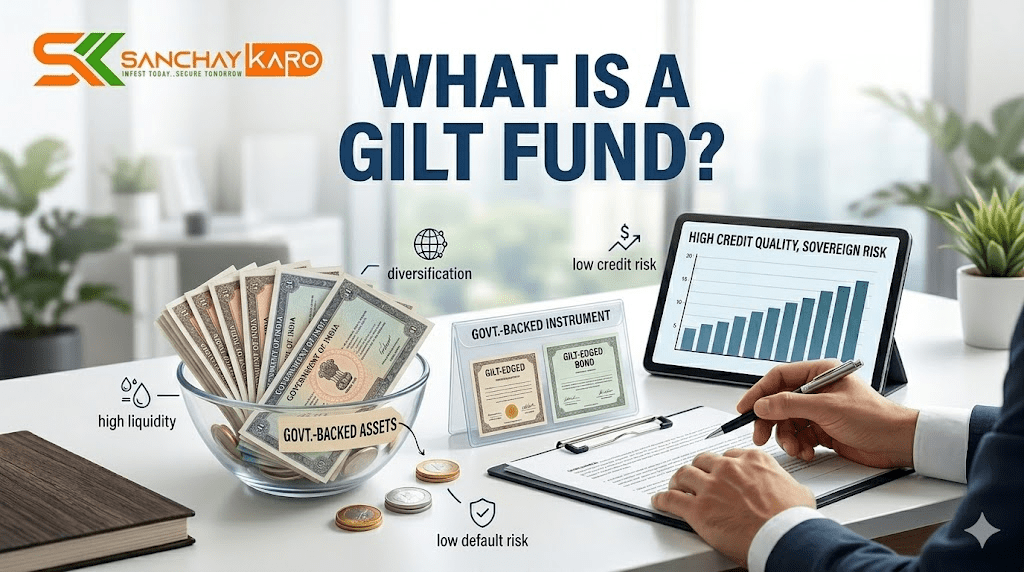

What is a Gilt Fund? – Complete Simple Guide for Beginners

Are you looking for a debt mutual fund that carries almost zero credit risk? A Gilt Fund could be the right choice for you. This blog explains what is a Gilt Fund in very simple language. You will also learn how to invest easily using the Sanchaay Karo app.

What is a Gilt Fund? (Very Simple Definition)

A Gilt Fund is a type of debt mutual fund that invests at least 80% of its total assets in government securities (also called G-Secs). These are bonds issued by the Central Government and State Governments of India.

Think of it like this: When you invest in a Gilt Fund, you are lending money directly to the government of India. Just like a fixed deposit lends money to a single bank, a Gilt Fund lends money to the government. Because the Government of India is the borrower, the chance of default (not repaying) is almost zero.

The name “Gilt” comes from old British times. The British government would issue bond certificates with a border of thin gold paint. Hence, they came to be known as ‘Gilt-edged’ certificates. In India, the first Gilt Fund was launched by Kotak Mahindra AMC in December 1998. Today, Gilt Funds collectively manage over ₹1.45 lakh crore, showing strong trust among both retail and institutional investors.

How Does a Gilt Fund Work? (Step-by-Step)

Gilt Funds pool money from many investors. A professional fund manager then invests that money in government securities. Here is how the whole system works:

Step 1: Government Needs Money

The government always needs money for roads, railways, defence, schools, hospitals, and other development work.

Step 2: RBI Acts as Banker

The Reserve Bank of India (RBI) acts as the banker to the government. The RBI collects money from banks, insurance companies, pension funds, and mutual funds on behalf of the government.

Step 3: RBI Issues Government Securities

In return, the RBI issues government securities (also called G-Secs). These are like IOUs (I Owe You) from the government. They come with a fixed interest rate (called coupon) and a fixed maturity date.

Step 4: Gilt Funds Buy These Securities

Gilt Funds buy these G-Secs on behalf of their investors. When the securities mature, the fund receives the principal amount along with the interest. This income is passed on to you, the investor, as returns.

How Do Investors Make Money?

Gilt Funds make money in two ways:

- Regular Interest Income: The government pays interest (called coupon) regularly. This provides a steady income stream.

- Capital Appreciation: When interest rates fall, the prices of existing bonds rise. This creates capital gains for the fund.

Key Features of Gilt Funds

Types of Gilt Funds in India

There are two main types of Gilt Funds in India:

1. Gilt Funds (Across Maturities)

These funds invest in government securities of different maturity periods. They can have short-term, medium-term, and long-term bonds in the same portfolio. The fund manager can move between different maturities based on the interest rate outlook.

2. Gilt with 10-Year Constant Maturity

These funds invest in government securities such that the Macaulay duration of the portfolio is always equal to 10 years. When bonds become shorter than 10 years, the fund manager buys new ones to keep the balance right. These funds are highly sensitive to interest rate movements because of their long duration.

According to SEBI’s classification system, Gilt Funds are listed as debt-oriented schemes along with other categories like Corporate Bond Funds, Banking & PSU Funds, Credit Risk Funds, and Floater Funds.

Benefits of Investing in Gilt Funds

Here are the main benefits of adding a Gilt Fund to your mutual fund portfolio:

Top Gilt Funds in India (2026)

Here are some of the best Gilt Funds in India based on AUM and performance:

| Fund Name | AUM (₹ Crore) | 1-Year Return (%) | 3-Year CAGR (%) | 5-Year CAGR (%) | Expense Ratio (Direct) | Modified Duration (Years) |

|---|---|---|---|---|---|---|

| ICICI Prudential Gilt Fund | 8,858 | 2.77% (2025 Q1) | — | — | 1.10% | 8.39 |

| Invesco India Gilt Fund | 252 | 0.11% | 6.55% | 5.31% | 0.46% | 9.33 |

| Quant Gilt Fund | 99.40 | — | 6.26% | — | 0.34% | — |

| Axis Gilt Fund | — | 1.22% | 6.51% | 5.28% | — | — |

| Nippon India Gilt Fund | 1,825.73 | — | — | — | 0.50% | — |

| PGIM India Gilt Fund | 95.06 | — | — | — | 0.67% | — |

Data sources: FundsIndia, Moneycontrol, Financial Express, PGIM India

Important Notes:

- Modified duration shows how sensitive the fund is to interest rate changes. ICICI Prudential Gilt Fund has a modified duration of 8.39 years, while Invesco India Gilt Fund has 9.33 years. Higher duration means higher volatility.

- Yield to Maturity (YTM) indicates current income potential. ICICI Prudential Gilt Fund has a YTM of 7.59%, and Invesco India Gilt Fund has a YTM of 7.01%.

Disclaimer: Past performance does not guarantee future returns. Please consult your financial advisor before investing.

Risks of Gilt Funds (Must Read Before Investing)

Gilt Funds are safe from credit risk but carry other significant risks. Every investor must understand these risks of Gilt Funds:

Real-world example: Gilt Funds underperformed in 2022 when interest rates rose sharply. Bandhan Gilt Fund delivered negative returns in certain quarters during that period. This shows that even government-backed funds can lose money in the short term.

Who Should Invest in Gilt Funds? (Ideal Investor Profile)

Gilt Funds are perfect for:

- Conservative investors who want zero credit risk but are willing to take some interest rate risk

- Investors with a long-term horizon of 3 to 5 years or more

- Investors who expect interest rates to fall – when RBI cuts rates, Gilt Funds perform very well

- Investors looking to diversify their portfolio – Gilt Funds have a low correlation with equity markets

- Risk-averse investors who want capital preservation with the potential for capital appreciation

- Investors who do not want to take credit risk but still want better returns than FDs

Who should AVOID Gilt Funds?

- Short-term investors with a horizon of less than 3 years

- Investors who cannot tolerate NAV fluctuations – Gilt Funds can be volatile in the short term

- Beginners who are new to debt mutual funds (start with liquid funds or ultra-short duration funds first)

- Investors who need guaranteed returns – FDs may be more suitable

- Investors who expect interest rates to rise – Gilt Funds underperform in rising rate environments

As Mint notes: “Investors with a higher risk appetite could consider a small tactical allocation to long-duration gilt funds—but only as a satellite exposure”. This means Gilt Funds should not be your entire portfolio; they should be a small part of your debt allocation.

Gilt Fund vs Other Debt Fund Categories

Many investors get confused between Gilt Funds and other debt fund categories. Here is a simple comparison based on SEBI rules:

| Fund Type | What It Invests In | Credit Risk | Interest Rate Risk | Best For |

|---|---|---|---|---|

| Gilt Fund | Government securities (80%+) | Zero | High | 3-5+ year horizon, falling rate environment |

| Banking & PSU Fund | Banks, PSUs, PFIs (80%+) | Very Low | Low to Moderate | 1-3 year horizon |

| Corporate Bond Fund | Corporate bonds (AA+ and above, 80%+) | Low | Moderate | 2-5 year horizon |

| Credit Risk Fund | Lower-rated corporate bonds (AA and below, 65%+) | High | Moderate | 3-5 year horizon |

| Floater Fund | Floating rate instruments (65%+) | Low | Very Low | Rising rate environment |

| Liquid Fund | Money market securities (up to 91 days) | Very Low | Very Low | Parking money for a few days/months |

Key differences to remember:

- Gilt Funds are the only debt fund category with zero credit risk. They are backed by the full faith and credit of the Government of India.

- Banking & PSU Funds represent a middle ground between the safety of government securities and the yields of corporate bond funds.

- Gilt Funds have the highest interest rate risk among debt funds because they typically have long durations.

Gilt Fund vs Liquid Fund – Which One is Better?

| Aspect | Gilt Fund | Liquid Fund |

|---|---|---|

| Primary Investment | Government securities (G-Secs) with long maturities | Debt securities with maturity up to 91 days |

| Credit Risk | Zero (sovereign-backed) | Very Low (invests in high-quality instruments) |

| Interest Rate Risk | High (sensitive to rate changes) | Very Low (short maturities provide protection) |

| Investment Horizon | Medium to long term (3+ years) | Short term (7 days to 1 month) |

| NAV Volatility | High – can fluctuate significantly | Very low – largely stable |

| Suitable For | Long-term goals, diversification, falling rate environment | Emergency funds, short-term parking |

As Kotak Mutual Fund explains: “Use Gilt Funds for long-term growth and exposure to government securities. Use Liquid Funds for emergency funds or short-term liquidity needs”.

When Should You Invest in Gilt Funds? (Timing Matters)

Timing is very important for Gilt Funds. They perform best during specific interest rate cycles:

| Market Scenario | Interest Rate Trend | Expected Impact on Gilt Funds | Investor Action |

|---|---|---|---|

| Falling Interest Rates | Downward | Bond prices rise → NAV increases → High returns | Best time to invest |

| Rising Interest Rates | Upward | Bond prices fall → NAV decreases → Low or negative returns | Avoid new investments |

| Stable Interest Rates | Steady | Returns moderate (mostly from interest income) | Hold existing investments |

| High Inflation Period | Rising (RBI increases rates) | Short-term losses possible | Stay cautious or invest in short-duration funds instead |

As 5paisa notes: “Constant maturity gilt funds tend to perform best during periods of falling interest rates. When the RBI cuts the repo rate, the yield on existing long-term bonds becomes more attractive, pushing up the price of those bonds, leading to capital gains”.

Gilt Funds in 2026 – What’s Happening Now?

The interest rate environment in 2026 is creating interesting opportunities for Gilt Funds:

- RBI has signalled stability after two years of rate hikes. When interest rates stop rising or start falling, bond prices rise – leading to capital gains for Gilt Fund investors.

- Experts predict a decline in interest rates in the upcoming fiscal year. This trend could benefit long-duration gilt funds, as bond prices generally rise when interest rates fall.

- Gilt Funds have seen quarterly returns of around 2.77% to 2.97% in Q1 2025 and Q1 2026 for some top funds.

However, as Mint advises: “Investors with a higher risk appetite could consider a small tactical allocation to long-duration gilt funds—but only as a satellite exposure. For most investors, shorter-duration, accrual-oriented funds may make sense as the core of their debt allocation right now”.

Taxation on Gilt Funds (Simple Rules for FY 2026-27)

Gilt Funds are treated as debt mutual funds for taxation purposes. The tax rules changed significantly from April 1, 2023.

| Purchase Date | Holding Period | Tax Treatment |

|---|---|---|

| On or after April 1, 2023 | Any period | Gains added to your income and taxed as per your income tax slab rate (no indexation benefit) |

| Before April 1, 2023 | Less than 3 years | STCG added to your income and taxed as per your slab rate |

| Before April 1, 2023 | 3 years or more | LTCG taxed at 20% after indexation benefit |

Key tax rules for FY 2026-27:

- Finance Minister Nirmala Sitharaman’s Budget 2026 speech brought no changes to debt mutual fund taxation, maintaining taxation at slab rates.

- Debt mutual funds purchased after April 1, 2023 are taxed at slab rates regardless of the holding period.

- Dividends (IDCW) are added to your income and taxed as per your slab rate.

- The fund house deducts 10% TDS under Section 194K if your dividend exceeds ₹5,000 in a financial year.

Important: The Association of Mutual Funds in India (AMFI) has requested the government to restore the indexation benefit for debt funds held for more than 36 months. If approved in future Budgets, this would make Gilt Funds more tax-efficient for long-term investors.

Example: If you fall in the 30% tax bracket and earn a capital gain of ₹10,000 from a Gilt Fund purchased after April 1, 2023, you will pay ₹3,000 as tax (30% of ₹10,000), regardless of how long you held the investment.

How to Invest in Gilt Funds Using Sanchaay Karo App

Now that you understand what a Gilt Fund is, the next step is investing. The easiest way is through the Sanchaay Karo app.

Sanchaay Karo is a simple, trusted, and SEBI-registered mutual fund investment platform. It helps you invest in top Gilt Funds and hundreds of other funds with just a few taps.

Why Choose Sanchaay Karo App for Gilt Fund Investment?

- Smart Goal-Based Investing: Tell the app your goal (retirement, child’s education, buying a house). It suggests the right Gilt Fund based on your risk profile and investment horizon

- Simple Dashboard: See all your investments in one place – no confusion or clutter. Track NAV, returns, and portfolio in real time

- Quick KYC: Complete your KYC online using Aadhaar and PAN in just 5 minutes. Paperless KYC is fully supported

- Start SIP from ₹500: You don’t need a lot of money. Start small with a Systematic Investment Plan (SIP) . You can do monthly SIP, weekly SIP, or daily SIP

- Track Performance: Get regular updates on how your Gilt Fund is performing against its benchmark (like CRISIL Dynamic Gilt Index)

- No Hidden Charges: Transparent and low-cost. You can choose between regular plan and direct plan options. Direct plans have lower expense ratios

- Stay On Track: Get timely reminders so your SIPs never stop

- Access to All AMCs: Invest in ICICI Prudential Gilt Fund, Invesco India Gilt Fund, Nippon India Gilt Fund, Quant Gilt Fund, Axis Gilt Fund, PGIM India Gilt Fund, and many more

Steps to Invest in Gilt Funds (Very Easy)

- Download the Sanchaay Karo app from Google Play Store or Apple App Store

- Sign up using your mobile number and email

- Complete KYC – upload PAN card and Aadhaar (fully paperless). You can also do video KYC if needed

- Search for “Gilt Fund” or let the app recommend one based on your financial goals

- Compare different Gilt Funds based on returns, expense ratio, exit load, modified duration, yield to maturity (YTM) , and fund manager track record

- Choose between lumpsum (one-time) or monthly SIP investment. For Gilt Funds, SIP is recommended to reduce timing risk

- Pay using UPI, net banking, or debit card

- Done! Your investment starts growing. You will receive regular statements

👉 [Click Here to Download Sanchaay Karo App Now] (https://apirrabbit.com/api/v1/master/LandingPage?arn=ARN-301757)

Important Tips Before Investing in Gilt Funds

Before you invest in a Gilt Fund, keep these points in mind:

- Understand the Interest Rate Environment: Gilt Funds perform best when interest rates are falling or expected to fall. Check RBI announcements, inflation data, and economic indicators before investing.

- Check Modified Duration: Modified duration shows how sensitive the fund is to interest rate changes. Higher duration means higher volatility. For Gilt Funds, duration can range from 5 to 10 years.

- Check Yield to Maturity (YTM) : YTM indicates the portfolio’s current income potential. Higher YTM means higher expected returns. Most Gilt Funds have a YTM of 7.0% to 7.6%.

- Have a Long Investment Horizon: Gilt Funds need at least 3 to 5 years to ride through interest rate cycles. Do not invest money you may need within 3 years.

- Use SIP, Not Lumpsum: A Systematic Investment Plan (SIP) helps reduce timing risk by spreading your purchases over time.

- Limit Allocation to 10-20% of Debt Portfolio: Gilt Funds should be a satellite part of your debt allocation, not the core. Most of your debt portfolio should be in accrual-oriented funds like liquid funds or ultra-short duration funds.

- Check Exit Load: Most Gilt Funds have nil exit load. But always check the Scheme Information Document (SID) before investing.

- Compare Expense Ratios: Direct plans have much lower expense ratios (often 0.30–0.50%) than regular plans (often 1.00–1.25%). Over time, this difference matters.

- Do Not Chase Past Returns: A fund that performed well last year may not repeat it. Look for consistency over 3-5 years.

- Avoid for Short-Term Goals: Gilt Funds are not suitable for emergency funds or money needed within 3 years.

Frequently Asked Questions (FAQs) About Gilt Funds

Q1: Are Gilt Funds safe?

A: Gilt Funds have zero credit risk because they are backed by the Government of India. However, they carry high interest rate risk. Your capital is safe from default, but your returns can fluctuate significantly.

Q2: Can I lose money in Gilt Funds?

A: Yes, you can lose money in the short term, especially if interest rates rise sharply. Gilt Funds can experience negative returns during rising rate environments. However, if you hold for 3-5 years, the chance of loss is lower.

Q3: What is the minimum SIP amount for Gilt Funds?

A: Most Gilt Funds allow SIP starting from ₹500 per month. Through the Sanchaay Karo app, you can start with as little as ₹500.

Q4: How much returns can I expect from Gilt Funds?

A: Historically, Gilt Funds have delivered 6% to 8% annual returns over 3-5 year periods. Over the past 15 years, the Gilt Funds category recorded 8.1% annualised returns.

Q5: What is the difference between Gilt Funds and Banking & PSU Funds?

A: Gilt Funds invest only in government securities and have zero credit risk. Banking & PSU Funds invest in banks and PSUs, which carry a small amount of credit risk but offer more stable returns and lower interest rate risk.

Q6: How are Gilt Funds taxed?

A: For units purchased after April 1, 2023, all gains are added to your income and taxed as per your income tax slab rate, regardless of the holding period.

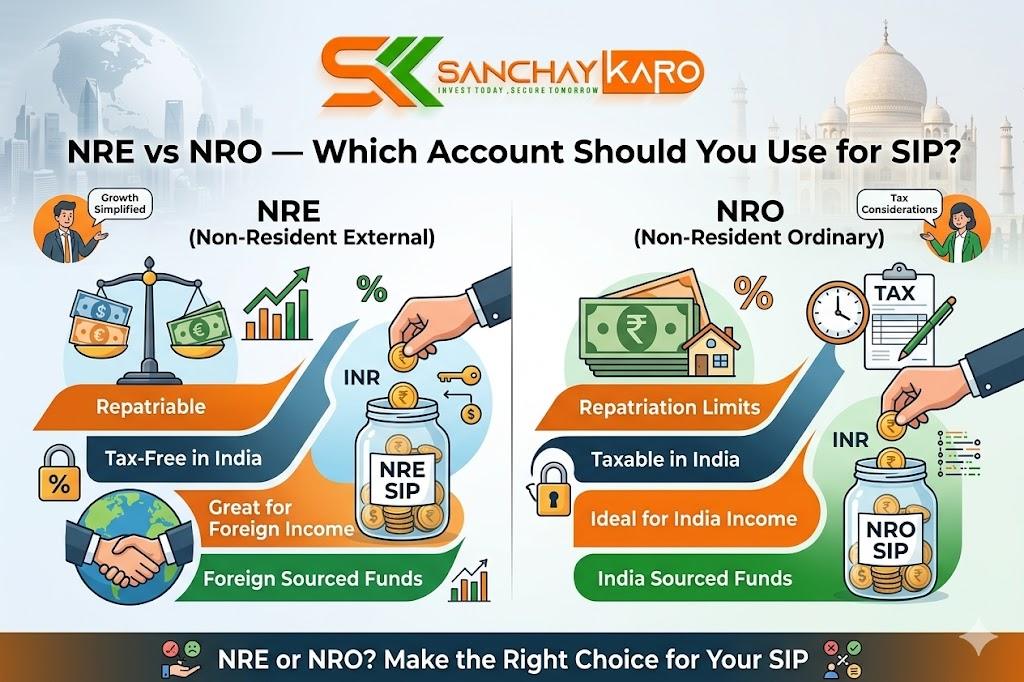

Q7: Can NRIs invest in Gilt Funds?

A: Yes, NRIs can invest in Gilt Funds through Sanchaay Karo app using their NRE/NRO account.

Q8: What is the expense ratio of Gilt Funds?

A: Expense ratios for direct plans typically range from 0.30% to 0.50%. Regular plans have higher expense ratios (often 1.00–1.25%).

Q9: What is the exit load for Gilt Funds?

A: Most Gilt Funds have nil exit load. For example, Invesco India Gilt Fund has an exit load of 0.00%.

Q10: Are Gilt Funds good for beginners?

A: Gilt Funds can be suitable for beginners who have a long-term horizon and understand that returns can be volatile in the short term. However, it is recommended to start with liquid funds or ultra-short duration funds first to understand debt fund basics.

Final Words – Should You Invest in a Gilt Fund?

Yes, if you:

- Are a conservative investor seeking zero credit risk

- Have an investment horizon of 3 to 5 years or more

- Expect interest rates to fall in the near future

- Already have a core portfolio and want to add diversification with Gilt Funds

- Are looking for potentially higher returns than bank FDs

- Can tolerate some NAV volatility in the short term

- Want to diversify your portfolio with an asset class that has a low correlation to equity markets

No, if you:

- Are a short-term investor with a horizon of less than 3 years

- Have a low risk tolerance and cannot tolerate NAV fluctuations

- Need your money back within 3 years

- Are looking for guaranteed returns – FDs may be more suitable

- Expect interest rates to rise significantly

Gilt Funds offer an excellent balance of safety (zero credit risk) and return potential (especially when interest rates fall). They are among the most transparent and well-regulated debt fund categories in India.

The golden rule for Gilt Fund investing: Understand the interest rate environment, check the fund’s modified duration, have a minimum 3-year horizon, use SIP to reduce timing risk, and keep them as a satellite (10-20% of debt portfolio), not the core.

Start your investment journey today with the Sanchaay Karo app.

👉 [Click Here to Download Sanchaay Karo App Now] (https://apirrabbit.com/api/v1/master/LandingPage?arn=ARN-301757)

Disclaimer: This blog is for educational purposes only. Mutual fund investments are subject to market risks. Gilt Funds carry interest rate risk and NAV volatility. Please read all scheme related documents carefully, including the Scheme Information Document (SID) and Statement of Additional Information (SAI) , and consult your financial advisor before investing. Past performance does not guarantee future returns. The Sanchaay Karo app is a platform for mutual fund investments; all investments are subject to market risk.